Wall Street Perspective

As Financial Farmers we must be wary of svengalis constantly whispering doom and gloom, because it is vital to have a long-term Wall Street perspective and remember all finance is behavioral finance.

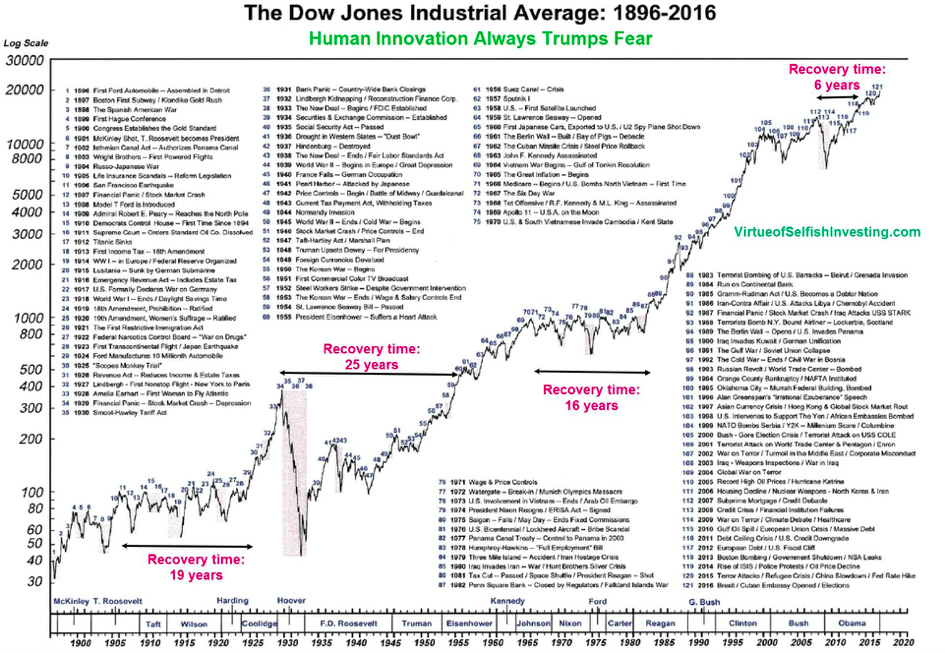

First, why is it vital to have a long-term Wall Street perspective? Over a long enough time period, as Zero Hedge has popularly quipped, we're all dead. BUT, a counterpoint to this morbid fact, is that innovation over time has propelled the economy and society to greater productivity. And the stock market has been along for the ride.

The second reason to question a svengali is that behavioral finance drives a LOT (most?) of the market's near-term volatility, trading, and returns. Sustained movements are the result of earnings, growth, innovation and major societal changes.

At this point in the economic cycle (most likely we're either in or on the cusp of a recession), the corporate picture isn't exactly bright. We've witnessed massive selloffs in tech companies and the only winners seem to be "boring" consumer staples anchored by a dividend. A lot of money has flowed out of the market into cash. Or real estate. So the bloom is off the rose for the time being.

For those entering the market, opportunity abounds. With multiple companies well off their highs and solidly into bear market territory. Many have been completely vaporized and sit some 60%, 70%, 80% or more off of their highs from just a couple months ago. For those who have been long-term holders, the past six months has been horrific, watching gains for the past two years getting destroyed. Even "blue chip" companies haven't been spared. Carnage is everywhere.

What's an investor to do? Stay focused on what matters; earnings, branding, growth, innovation, integrity, and cash flow. Have emergency cash on the sidelines. Look for opportunities and be patient. The last bit is perhaps the hardest. Many older investors in the stock market don't think they'll live to see a Bull Market again. But it is hard to believe that this great country, which has weathered so much in the past, could be permanently hobbled by inept leadership today for very long. So we're in a waiting game now.

Similar to economic cycles, the political pendulum swings and very few Presidents or political parties survive recessions intact. New blood focused on innovation, growth, and stability rises to the moment. Remember dear readers, the business of America is business. In the meantime, a fallow field presents many, many opportunities for a farmer with a keen eye.