Recession Game Plan

Right on time for the long weekend's glorious

4th of July celebration is a self-inflicted

recession. Here at ILAF we don't point fingers, we know who owns this debacle and our job is to help readers put together a game plan for this recession.

First, what is a recession? A recession is an economic contraction defined technically by a very specific course of events; two quarters of negative gross domestic product readings from the

U.S. Bureau of Economic Analysis.

The Atlanta Fed's GDPNow gauge sees the second-quarter coming it at -1%. As a quick recap, the first-quarter was -1.6%. So we're there. The "official" number for Q2 will be released on July 28th. Expect it to trend worse right up until the release as the cart long-ago lost its wheels. Many a disgruntled farmer is careening down a pot-holed road without all his wheels, a tank full of $5 gas, and consumers cutting their spending. But I digress.

Game plan readers, a game plan! OK first let's get real. The "best" economists in the world didn't predict a recession, and IF we were to get one at all silly taxpayer, it wouldn't hit until AT LEAST 2023! Ahhh...is there a way to revoke a PhD in economics? If the "best' economists got this obvious truth wrong, can we put much faith in their assurances that this will be a "short" recession? No, we can not.

Keep in mind, some 30-40% of the US population is pretty much immune to an economic downturn; meaning that they are on fixed incomes of one sort or another; Social Security, Pension, and/or Union jobs with fixed (but increasing) salaries. Why does this matter? The true effects of this recession will dissipate slowly and linger longer than predicted. I suspect 18 months of pain await us.

Typically, credit tightens during a recession as rates increase. Check that box. The Fed has been busy as a bee raising rates. Mortgage rates have nearly doubled in the course of a year. Remember, the Fed's mandate is to "ensure price stability and steady inflation of 2%." Meaning? There is more pain to come. With inflation at 8.6% "and rising" as

Johnny Cash would sing, the Fed is hellbent on increasing rates. Expect another 75 basis points (0.75%) at the next meeting 26-27 July and then again on Sept 20-21.

So for those who are cash flush, laddering CDs seems to make sense especially if you're keeping it short term. Who knows, given the desire to crush inflation we might see Fed Funds rates at 5% by the end of this year. That would imply mortgage rates over 8%.

The major takeaway from the Fed action is that they are directed (and determined) by the current Administration to break inflation. The optics are horrible with gas, food, and housing prices soaring. What this means for stock investors is that they are not particularly concerned with collateral damage (read your 401K, brokerage account, etc.)

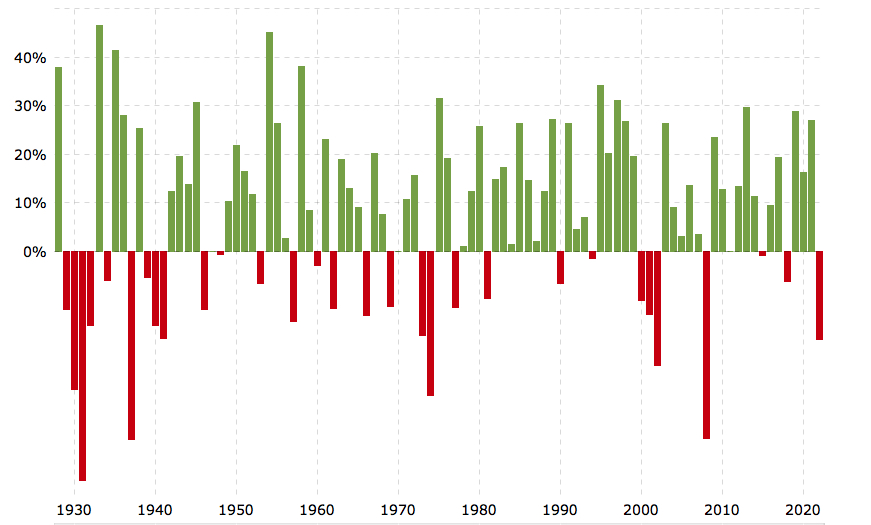

This ties back into the Social Security, Pension, and Union paragraph above. Some 30-40% of Americans are completely immune to the effects of a crashing market. Consider, this year's start in the stock market (3 Jan - 30 June) was the worst since 1964. In the bond market it was the worst since 1842. You read that correctly. 180 years. So if you think we have a problem, you are correct.

In a recession, typically the non-union employees, jobs, and businesses will be shed first. So late hires, job hoppers, recent business startups, etc. are most vulnerable. A recession by definition means to "recede." Commercial sector spending will also be the first hit. Public sector is still flush with excess tax returns and largesse from Covid to the

tune of billions.

So stock investors have a handful of viable choices; if the goal is to survive, then the companies with the strongest balance sheets, best brands, and inflation pricing power offer better chances than say a company with lots of debt or leverage, emerging branding, and cut-throat pricing.

Much of the economic pain we're experiencing is directly due to the price of oil and the corresponding cracking into gasoline. The insistence of pushing ahead with a green agenda without a transition bridge via fossil fuel has been a disaster, and the global economy will also get caught in this contagion. As with most supply-demand scenarios, oil demand, especially with $5 gas the norm across America now, should begin to wane. Consumers will aggressively change their spending habits when they run dry of excess Covid liquidity.

As you read this blog right now, demand priorities are already shifting. Consumption choices are changing. The "trickle down" effects of a recession will hit the private sector, in particular small businesses which account for

the majority of employment in this country, the hardest first. Next hit will be the larger private companies. Then public companies. In reality, a recession works more like a "trickle up" scenario, the only think I know that defies gravity.

Middle Class taxpayers get hit worst and first.

Depending on where you are on the socioeconomic spectrum plan accordingly. If you're a small business owner or employee you are most vulnerable. Consider cash flow and liquidity as your most important priorities.

Being dead is bad for business. Survival is paramount.

If you're a mid-size business owner or employee consider the durability of your brand and the value you offer as vital resources. Is what you offer elastic or inelastic? Are you customer obsessed? A merger or takeover of a smaller rival might make sense here.

If you're an employee of a larger corporation, ensure you aren't on the chopping block and maximize your utility. Are you taking advantage of all your employer benefits? Are you indispensable?

Local, State, and Federal employees should weather the storm well, in fact this is an opportune time for them to actually pick up distressed assets on the cheap. Blood in the streets has typically been a good time to buy. Get ready to pounce on distressed asset sales from your fellow citizens laid low by the recession.

Our government should be the least affected, at least initially, by its own policies. But by 2023 the effects will be apparent as withholdings in 2022 are already falling for almost everyone "on the economy" and capital "gains" will most likely non-existent for most filers.

Expect the full pain of the recession to kick in high gear later this year. Even though over the past 6 months we have witnessed the largest destruction of wealth in the course of human history, I believe we are only in the eye of the storm now. Think about that for a moment. "

Paper Loss" or not, wealth destruction hurts for real with destabilizing "trickle" down effects. Bidenomics will have a lasting impact on the United States for generations to come.